NewGeography.com blogs

Since October 2008 I’ve been writing here about problems in mortgage backed securities (MBS). There is more evidence surfacing in bankruptcy courts that the paperwork for the underlying mortgages wasn’t provided correctly for the new bond holders, leading to delayed or denied foreclosure proceedings.

New York Times’ Gretchen Morgenson is reporting new successes in cases from Florida and California. A judgment on a home in Miami-Dade County (FL) was set aside on February 11 when the new mortgage holder could not produce evidence that the original mortgage lien had been assigned. In one of the California cases, the lender tried for foreclose on a mortgage that had previously been transferred to Freddie Mac!

The earliest decision I’ve seen is from Judge Christopher A. Boyko in Cleveland. Plaintiff Deutsche Bank’s attorney argued, “Judge, you just don’t understand how things work.” In his October 31, 2007 decision to dismiss a foreclosure complaint, Boyko responded that this “argument reveals a condescending mindset and quasi-monopolistic system” established by financial institutions to the disadvantage of homeowners. The Masters of the Universe were anxious to pump out mortgages into MBS so they could continue to earn fees – making money at any cost.

One element of the newest Homeowner Bailout program is to allow bankruptcy court judges to modify mortgage loans. If the types of cases decided in OH, FL and CA continue to spread, that may not be necessary. The first question in any foreclosure procedure will become: can you prove a lien?

This raises further questions about those “toxic assets” that Geithner and Bernanke are so anxious to buy up at taxpayer expense. According to the Morgenson article, some MBS holders are trying to force the mortgage originator to take back the paper. However, many of the worst offenders are already defunct.

How far can the totals go? Federal Reserve Chairman Ben Bernanke testified before the Senate Budget Committee on March 3, 2009. He believes that the markets will be “quite able” to absorb the debt issued by the US government over the next couple of years to cover all the bailout and stimulus payments “if there is confidence that the US will get it [the economy] under control.” When Senator Lindsey Graham (R-SC) suggested an “outer limit” at which the national debt was three times gross domestic product, Bernanke said that “it wouldn’t happen because things would break down before that.” They’ll be lending to homeowners who have higher debt ratios than that. Frankly, I’d rather lend to the US government at that ratio, and I suspect a lot of investors – both domestic and foreign – feel the same way.

On the one hand, Bernanke spoke like a “Master of the Universe” when he told the Senators that he wasn’t worried that printing all this extra money would generate future inflation. He said that when the economy begins to grow again, the Federal Reserve is “very comfortable” they will be able to deflate their bloated balance sheet. On the other hand, he did not sound like a Federal Reserve Chairman when Bernanke said “We don’t know for sure what the future will bring.” Of the two Bernankes I like the second one better: no one knows exactly what the future will bring. Why pretend that you know what the best action to take three years from now will be – or what impact it will have. I find it disconcerting, to say the least.

There are a few things we can watch for in the coming weeks and months. The President’s budget came out yesterday and will go through Congress now for approval. Don’t get too distracted by it though – virtually everything in it can change. Instead, work with what you know. The stimulus package was passed and the states are getting details now on how much and for what they can expect money from Washington. Focus on where that money is going. The best way to minimize the damage being done by the Federal Reserve’s printing presses is to be sure that money is spent in the real economy. That means roads, bridges, schools, sewer systems – and not research and development on sources of alternative fuel or studies on global warming. We are in the middle of a crisis. This is not the time to spend on wishes and dreams. If the money is spent on real infrastructure projects, it can help to mitigate the potential inflationary effects later.

The Treasury and the Federal Reserve have no choice but to keep their foot planted fully on the accelerator. Setting infrastructure in place now means we’ll get good traction later when the economy starts moving forward.

Paris Mayor Bertrand Delanoë has spent much of his first term in implementing measures to restrict car use. Delanoë took many lanes of road traffic away from cars and turned them into exclusive bus and taxi lanes. This had virtually no effect on public transport use, according to University of Paris researchers who also found as a result that traffic congestion worsened, greenhouse gas emissions increased and overall cost to the Paris economy of more than $1 billion annually.

Now the Mayor is establishing a car hire program that will make electric cars available throughout the ville de Paris at electric charging stations. Initially 4,000 cars will be involved in the “Autolib” program. London Mayor Boris Johnson has announced plans for a similar program. These are healthy developments and a further reflection that preferred lifestyles can continue, while still reducing greenhouse gas emissions.

From late-night refrigerator raids to splurging on a new wardrobe, everyone is prone to the occasional overindulgence. For San Francisco Mayor, Gavin Newsom, that overindulgence meant nothing more than a plastic water bottle.

In June 2007, the mayor “issued an executive order directing city government to no longer purchase bottled water,” to cut down on waste in the city landfill and to utilize the pristine Sierra Nevada reservoir’s resources.

Last year, Newsom also called on restaurants to stop selling bottled water to customers and has generally declined bottled water at most events.

In something better suited to cushy celebrity gossip rags, an empty case of Crystal Geyser Alpine Spring Water was discovered in the mayor’s trunk of his car.

While a spokesman for the mayor has assured the public that the water was for the mayor’s security detail, the Newsom camp also issued a statement that would be better suited for rehab-bound celebrity.

“The mayor will be the first to admit that he occasionally indulges in bottled water,” said his spokesperson. “It’s not something he’s proud of.”

During these bleak economic times, the public’s hyper-vigilant scrutiny of politicians seems zeroed in on busting them on seemingly inevitable examples of hypocrisy.

Needless to say, Newsom will think twice before purchasing bottled water again.

Looking for a safe haven for your banking investments? The Royal Bank of Canada is about three times the size of Citigroup, Royal Bank of Scotland or Deutsche Bank – and they haven’t cut their dividend in more than 70 years. Although Canadian banking profits declined double-digits last year, they actually had profits. Pretty much the rest of the world’s banks are reporting massive losses.

It seems the folks above the 49th parallel have been fiscally responsible. According to a story on Bloomberg.com “not one government penny” has been needed to support any Canadian bank “from British Columbia to Quebec” since the financial meltdown began in 2007. Not that the Canadian government left them out in the cold, either. A $C218 billion fund was set up last October – ostensibly to be sure Canadian banks could compete in international markets with all the government-backed banks in the rest of the world – but none of the banks took any of it.

According to Bloomberg, European governments “committed more than 1.2 trillion Euros ($1.5 trillion) to save their banking systems from collapse.” As close as I can tell, between the Federal Reserve and Treasury, the US has poured over $3 trillion down the drain of financial institutions.

(To understand the complications in calculating an exact U.S. amount, see my earlier articles for more information on how the Federal Reserve Bank of New York, under now-Secretary of the Treasury Tim Geithner, funneled money through Delaware limited liability companies to non-bank entities.)

Only 7 banks in the world have triple-A credit ratings – 2 of them are Canadian. While the rest of the developed, industrial nations are pouring hundreds of billions each down the black hole that is their financial systems, our Neighbors to the North were engaging in “solid funding and conservative consumer lending.”

Canada is the only member of the G-7 to have balanced their budget 11 years in a row. Immigrating to Canada is looking like a better idea all the time.

For some time it has been assumed that reducing greenhouse gas (GHG) emissions will require a shift to cars that do not use petroleum and to power plants that do not use coal, because of the emissions from these sources. All of this may be a false alarm.

Two recent articles indicate that there may be no need to reduce petroleum use in cars to reduce greenhouse gas emissions (GHG). The first story from USA Today describes a new process for producing gasoline from CO2. If implemented, this could materially reduce GHG emissions from coal fired electricity plants – a principal source of GHG emissions in the United States and in many other nations, including China and India. Another story in The New York Times, indicates the potential of technology that could capture CO2 emissions from cars, to be later refined into gasoline. All of this is further evidence that technology is the answer with respect to reducing GHG emissions.

Banks in Connecticut, once interested in accepting funds from the Trouble Asset Relief Program, are now “questioning whether it’s worth participating in the program.”

Concerns over the undefined terms and changing conditions imposed on those accessing TARP money has made the banks uneasy about such long-term commitments.

President and CEO of Connecticut River Community Bank, William Attridge, said that the fundamental problem with the program is its open-endedness and the reliance on total-compliance from the banks regardless of any future changes.

President Obama and members of Congress “are under public pressure to toughen conditions on the TARP money in order to improve the poor public image.”

The TARP program was originally created with the intent to “revive bank lending” according to Treasury officials. However, with the obscure terms and conditions currently associated with the program, some argue we’ve lost sight of TARP’s original purpose.

With approximately $293.7 billion in TARP funds distributed as of Jan. 23, undefined regulation doesn’t have all banks protesting.

Some smaller bank feel that increased capital will help the banks “continue to steal market shares from larger banks and help offset inevitable weaknesses among borrowers due to the recession.”

It remains to be seen whether or not the Connecticut bankers will take TARP money, but too many unknowns and perceived risks will certainly be factors in its approval.

Don’t worry about China taking over the US economy. Despite what all the talking heads on TV and the radio talk shows are saying, there isn’t another country out there that hasn’t been hammered at least as badly as we have by the financial meltdown. The problem with any other country attacking the US dollar, for example, is that they are all holding a lot of US dollars. You probably remember last year they were worried about the fact that we import so many goods that we have big “trade imbalances” – meaning that we buy more of their goods than they buy of ours.

Now remember this: we pay for those imports with dollars. So, again, if the dollar is worth less (or worthless) then they are not going to be getting as much for their imports. Raising the price of their goods, that is, simply charging more dollars won’t do them any good either. We’re in a recession, and Americans are tightening their belts. Demand for imported goods, like demand for all goods except luxury goods, is price sensitive. The more they charge, the less we buy. According to an article on CNN.com, our belt tightening has ended the “Road to riches for 20 million Chinese poor.”

Furthermore, it’s in the best interest of countries around the world that the US dollar stays strong. The door does swing both ways. According to Jack Willoughby at Barrons.com, “European banks provided three-quarters of the $4.7 trillion in cross-border loans to the Baltic countries, Eastern Europe, Latin America and emerging Asia. Their emerging-markets exposure exceeds that of U.S lenders to all subprime loans.”

To support all of that exposure, the European Central Bank has been obtaining dollars from the U.S. Federal Reserve in currency swaps. The value of these swaps, where dollars are exchanged for other currency at a fixed and renewable exchange rate, went from $0 to $560 billion this year.

And the Federal Reserve printing presses keep rolling along.

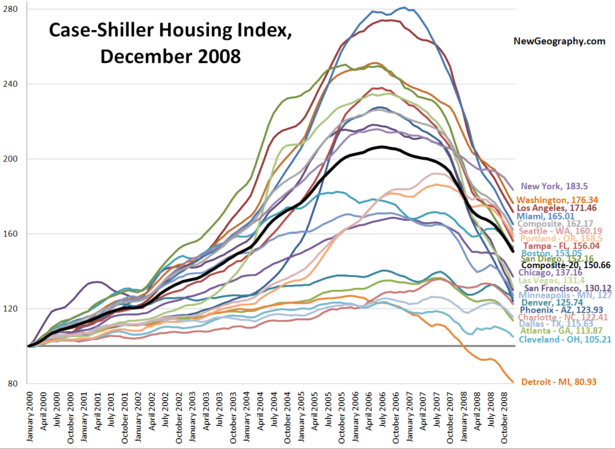

S&P released the December Case-Shiller Housing Price Index data this morning: no market has been spared from the free fall. Steep price declines continue in ultra-bubble regions Las Vegas, Miami, San Diego, Phoenix, and Las Vegas. Even the relatively healthy markets of Charlotte, Dallas, and Atlanta have been sliding since mid-2008. Here's the line chart:

Cleveland is seeing the slowest decline, but that isn't saying much. My pick for healthiest markets? Denver, where prices are still up 25% from the 2000 baseline but still down 5.2% from the most recent upswing in July 2008. And Dallas, down 6.1% from the July 2008 peak and down 8.6% from June 2007. Dallas is up 22.9% since the Jan 2000 baseline.

Follow this link for a bigger version of the chart.

In the ten-year stretch from Sept. 1929 to Sept. 1939, spanning the worst years of the Great Depression, the stock market dropped a full 50%, adjusted for inflation. Look out, the current decade (Feb. 17, 1999 to Feb. 17, 2009) appears to yield the same decrease: the Standard & Poor’s 500 stock index is down roughly 50%, also adjusted for inflation.

But this difficult period has not been all skull and cross-bones: six-month certificates of deposit “have yielded a real total return of roughly 12%” and the value of residential homes in large cities has increased 30% over the same period, according to Business Week’s Michael Mandel.

With many investors' savings sitting in once-promising equities, the question of whether to stay in stocks or bail out is on many people’s minds.

Staying in stocks could decrease the value of your investments to the point that they “may never reach their original value, much less show a profit.”

On the flipside, bailing out and going into safer assets says “you are giving up on any potential of an upside” if the market has a big rebound.

The market will always fluctuate and whether your glass is half-empty or half-full, and long term history says more growth is ahead. But as they say on TV, “past returns are no guarantee for future performance.” How much are you willing to bet on the long-term future of the US economy?

|

{kind=link}